As the old saying goes, “death is the great equalizer of human beings.” It’s a fundamental component of the human condition, and an experience we will all one day share. But, for many, it can also be an uncomfortable and even taboo subject.

Talking about and planning for death may feel uncomfortable at first, but it can ease your anxiety about the future and provide clarity as you determine what’s important to you. Most importantly, it helps you protect and provide for the people you love.

Why is end-of-life planning important?

End-of-life planning is the process of making decisions and getting your affairs in order in preparation for when you pass away. This includes important decisions about your property, healthcare, finances, and more.

By creating an end-of-life plan, you can relieve your family members of a huge administrative burden. Think of end-of-life planning as a final gift you leave for your loved ones. By taking time now to make tough decisions about your health and finances, you prevent that burden from being shifted to them after you die.

Often, when we reach the end of our lives, we don’t have the capacity to express what we want to happen at a time when that information is the most important. That’s where end-of-life planning comes in. By creating legal documents and discussing your wishes with your doctors and loved ones in advance, you can help ensure your wishes are followed in pivotal moments and your loved ones are taken care of.

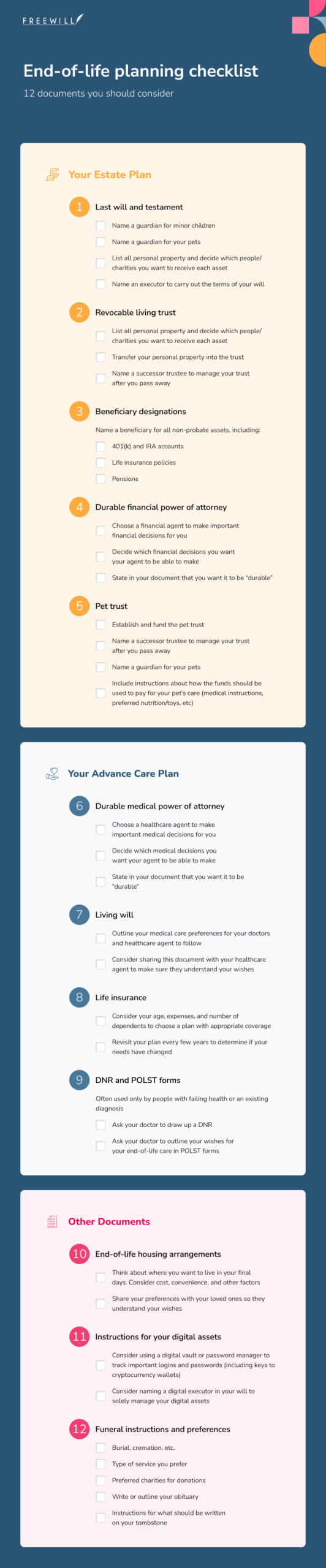

Below we’ve created a guide of 12 important documents you should consider as part of your end-of-life planning checklist. You can also download and print our end-of-life planning checklist for future reference.

1. Last will and testament

In your will, you specify who you want to receive your property after you pass away. This includes physical assets — like your home, vehicles, and possessions — and your financial assets, like your bank and investment accounts. The people or organizations you name to receive your property are called beneficiaries. Having a will streamlines the probate process and makes sure your assets go to the people you want to have them.

With a will, you can name a guardian for your minor children and outline who should care for your pets. You’ll also use your will to name an executor, who is the person responsible for following the instructions in your will and distributing your estate to your heirs after you die.

There are many ways you can make a will. For people with simple estates and wishes, a do-it-yourself online will can be a great, affordable option. For example, you can use FreeWill’s online will-maker to create your free, legally-valid will in just 20 minutes.

2. Revocable living trust

Like a will, a revocable living trust (RLT) is a tool you can use to manage and distribute your property after you pass away. But unlike a will, a RLT is a legal entity, meaning it's able to “own” property. Once you set up a RLT, you’ll transfer your assets to it so the trust is the owner. Then you can be the trustee — the person overseeing the trust — so you’re still able to use and manage the property.

When you set up a RLT, you should name a successor trustee who will manage the trust assets when you become disabled or pass away. You should also choose beneficiaries to receive the trust property after you die.

RLTs need more management than wills because you have to transfer new property to them as you acquire it, but they come with some advantages as well. For example, assets in a trust can avoid going through probate (the legal and court-driven process of distributing your assets), which can save your family time and maintain privacy. With a trust, you can skip probate and streamline the process of transferring your assets to your beneficiaries.

You have the option to create a revocable living trust using FreeWill’s online software.

Not sure whether a RLT or a will is the best fit for your end-of-life plan? Learn more about the differences and how to choose the best option for you. Even if you create a RLT, you should still have a simple will. These “backup” wills for RLTs are called pour-over wills. Learn more about pour-over wills and how they help safeguard your assets.

3. Beneficiary designations for non-probate assets

There are certain assets, called non-probate assets, that can skip probate and transfer directly to a beneficiary when you die. 401(k) accounts, pensions, and life insurance policies are all examples of non-probate assets.

To set beneficiaries for these assets, you have to fill out a specific beneficiary designation form from the institution where you have the asset (for example, your life insurance provider). Because of this separate process, you shouldn’t list these assets in your will.

Each institution has its own beneficiary designation form, so make sure you fill out the correct forms for the assets you own. FreeWill offers a free online platform where you can designate your beneficiaries quickly and easily, all in one place.

4. Durable financial power of attorney

With a financial power of attorney (POA), you choose someone to make important financial decisions for you if you can’t make them yourself. This could include paying for your medical expenses, filing your taxes, and more. The person you name in your financial POA to make these decisions is called your agent.

There are many different ways to use a financial POA. For end-of-life planning, you’re preparing for a situation where you may be incapacitated (for example, if you were in a coma). For this purpose, you want your financial POA to be “durable,” meaning your agent’s authority continues if you become incapacitated.

Having a financial POA ensures someone is handling your finances if you can’t manage them yourself. This could be crucial if, for example, you have loved ones who rely on you to pay bills or manage the household.

You can use online software, like FreeWill, to create a durable financial power of attorney for free.

5. Pet trust

Even though they often feel like family, pets are considered property by the law. That’s why it’s important to have a plan for them in case you pass away. If you don’t, they may end up with whoever is willing to care for them. If no one steps up or is fit to care for them, your pets could be placed in a shelter.

To avoid this, you can choose a caregiver for your pets in your will, and even set aside some money to pay for the cost of their care. If you want to be sure your pets are cared for in a certain way after you die, you may take this one step further and establish a pet trust.

Just like a trust you set up for human beneficiaries, you can establish a trust for any pets you own. With a pet trust, you fund the trust with assets that will pay for your pet’s care. You can also include instructions for the trustee about how the funds should be used. For example, you can list your pet’s required medical treatments or favorite toys.

A pet trust may be a good option if you:

- Have a pet with a long lifespan, like a parrot or horse

- Have a pet that is expensive to care for, or has special needs

- Want to offset the cost of caring for your pets

You can learn more about pet trusts from the ASPCA.

6. Durable medical power of attorney

With a medical power of attorney (POA), you choose someone to make medical decisions for you if you can’t make them yourself. These decisions could be about your treatment options, surgery, medication, and end-of-life care. The person you choose to make these decisions is called your healthcare proxy or agent.

Having a medical POA ensures that someone you trust can make critical decisions for you about your health if you’re ever unable to. Before you nominate a healthcare agent in your medical POA, you should confirm that the person is willing to serve. Once they agree, make sure that they understand your wishes.

7. Living will

Despite its name, a living will isn’t the same as a last will and testament. A living will is a document that lets you outline your healthcare preferences in the event you can’t communicate them yourself. You can state your wishes about the medical treatments, medications, and procedures you do or do not want to receive.

If you have a living will and a medical POA, these documents can work together: the decisions your healthcare agent makes must align with the wishes in your living will. When combined, these two documents are sometimes called an advance healthcare directive (AHCD).

By having an AHCD in place before you need it, you can give your loved ones direction and insight even in moments when you can’t communicate your wishes. With FreeWill’s online software, you can create your AHCD (medical POA and living will) for free.

8. Life insurance

If you don’t already have life insurance, it may be worth considering as part of your end-of-life plan. Life insurance helps protect the people who rely on you financially if you were to pass away. The payout from a life insurance policy can be used to cover your family’s day-to-day and long-term expenses. It could also be used to pay for expenses that accompany death, like your funeral or probate costs.

To decide how much coverage you need, consider your current age and your household’s expenses. To buy a life insurance policy, you can research providers online and request a quote. Many employers also offer life insurance coverage as a benefit, either for free or at a reduced rate. Consider sitting down with a life insurance agent or licensed representative if you need help determining your needs and options.

9. Do not resuscitate order and POLST forms

If your health is declining, you may want some additional forms in your end-of-life care plan to outline your wishes about life-saving treatment. A “do not resuscitate order,” or DNR, tells healthcare providers you don’t want to be resuscitated in the event of an emergency. A POLST — Physician’s Orders for Life Sustaining Treatment — outlines your wishes for end-of-life care, especially in regards to an existing diagnosis.

Both of these documents are often used by people with failing health and usually aren’t necessary if you’re healthy. To create these forms, talk to your doctor. They’ll work with you to record your wishes and put them on file at your hospital.

10. End-of-life housing arrangements

Even if you’re healthy and independent now, it’s worth considering where you may want to live in your final days. For example, would you prefer to live in a nursing home or receive in-home care from a caregiver? Or perhaps you intend to move in with family members, like your adult children.

Think about the costs and tradeoffs associated with each living arrangement. Speak with your loved ones about your wishes to make sure you’re all on the same page.

11. Instructions for your digital assets

The average person under 70 has nearly 200 digital accounts. Many of these are important assets like bank, investment, and insurance accounts that will need attention when you pass away.

You can use a digital vault or password manager to keep track of your logins and passwords, and choose who should have access to them after you die. You can also name a digital executor in your will who will manage and shut down your online accounts. In FreeWill’s will-making forms, we include a section where you can list out and name your digital accounts.

If you own cryptocurrency assets, it’s crucial that you leave behind instructions detailing which coins you own, where they’re stored, and how to access them. Cryptocurrencies are not treated the same as other financial assets, like bank accounts, which can be transferred to your beneficiaries after you die. If you lose the private key to your crypto assets, those assets can likely never be recovered. That’s why it’s important to include instructions on how to access them in your end-of-life plan.

12. Funeral instructions and burial arrangements

It may seem morbid, but there are several benefits to planning your own funeral. Planning ahead reduces the emotional burden on your loved ones. Every decision you make now is one your family doesn’t have to make during a time of deep grief.

In your funeral instructions, you can state whether you want to be buried or cremated, what type of service you’d prefer, where you’d like to be laid to rest, and more. You can also choose a preferred person you want to carry out your instructions, like a spouse or child. You could even write your own obituary, or note what you want included in it.

Funeral instructions aren’t considered legally-binding documents, but they’re extremely helpful and appreciated by loved ones. In FreeWill’s will-making forms, we include a separate section where you can list your funeral preferences. You can also list any charities that you would like your loved ones to support in your memory.

I’ve completed my end-of-life plan — now what?

- Store your documents in a safe place. Let your will executor, power of attorney agent, and other important people know where they are. Be sure to keep them informed about any changes.

- Talk to your loved ones about your wishes. This may be difficult or uncomfortable at first, but remember that planning ahead is the kindest thing you can do for the ones you love.

- Keep your documents up-to-date with your latest wishes. Revisit your end-of-life planning documents every three to five years, or whenever you experience a big life event (like the birth of a child or grandchild). You may want to revisit your documents more often if you are near the end of your life or have a terminal illness.

- Consider meeting with a lawyer if you have questions about your legal documents. Preparing an outline of your wishes in advance can save you time and money in attorney fees.

End-of-life planning is a gift to your loved ones

While it may be uncomfortable at first, putting together an end-of-life plan is one of the most thoughtful things you can do for the people you love. Death is inevitable. By preparing for it, you can gain a deeper appreciation for what matters to you, and protect the people you love in the process.

You can download and print our end-of-life planning checklist here. To help you get started, FreeWill offers several end-of-life planning forms that you can fill out for free online. Choose one and have a valid, legally-binding document in just 20 minutes. Get started today.

Make your free estate plan today

Make your free advance healthcare directive

Make your free durable power of attorney

Make a stock donation today

Make your free revocable living trust