When you pass away, it’s likely that some of what you own will go through probate before being passed on to your loved ones. Probate is the legal process of administering your estate after you die. A court oversees the process to make sure your debts are paid and your property is passed on to the right people. Probate typically takes between six months and two years, and in some states the court and legal fees can be costly.

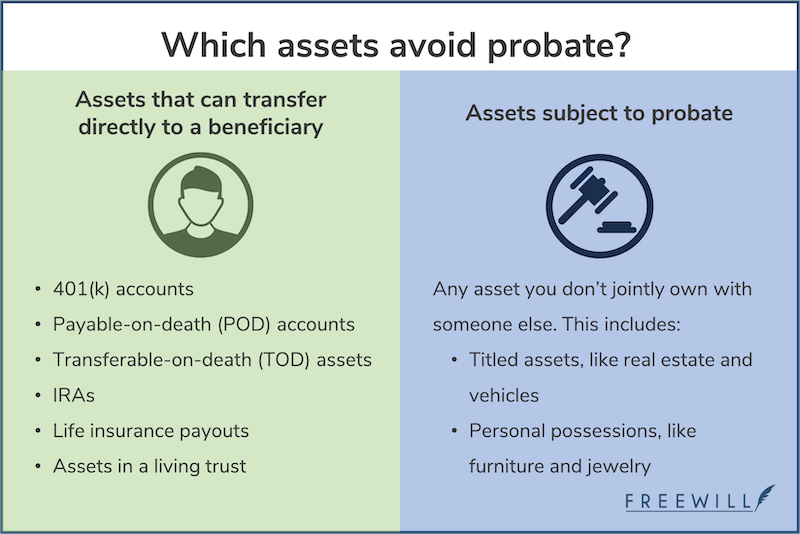

However, there are some assets that don’t have to go through the probate process to be passed on to your family, friends, or chosen organizations (like your favorite charity). These are known as non-probate assets. Some examples of non-probate assets include:

- 401(k) and IRA accounts

- Life insurance policy payouts

- Certain bank and brokerage accounts

To prevent non-probate assets from going through probate, you have to choose a beneficiary for each of them using a beneficiary designation form. Then, after you die, ownership of these assets can smoothly transfer to your beneficiaries — avoiding the probate process.

What is a beneficiary?

In this context, a beneficiary is a person or organization you choose to receive the benefits of a non-probate asset (for example, the payout from your life insurance policy).

You can name different beneficiaries for each asset — it doesn’t always have to be the same person or organization. For many non-probate assets, you can also name more than one beneficiary and specify the percentage each should receive. For example, perhaps you have two children, and you want the payout from your life insurance policy to be split equally between them. In that case, you would state that your children should receive equal shares of the payout.

Your primary beneficiary is the first person you want to receive an asset after you pass away. You can also name contingent beneficiaries (or secondary beneficiaries). Your contingent beneficiary will receive the asset if your primary beneficiary can’t or won’t. For example, perhaps your primary beneficiary passed away before you, and you didn’t update your beneficiary forms before you died. That asset will now go to your contingent beneficiary. If you didn’t list one, the asset may have to pass through your estate as part of the probate process.

Some institutions will list a default beneficiary for you if you don’t list one yourself — usually a spouse or child. But not all institutions will, and you shouldn’t rely on this default designation when you could choose one yourself.

You should designate at least one beneficiary for each of your non-probate assets. And since your beneficiary designations override what’s written in your will, it’s important to keep them up to date.

Who can you designate as a beneficiary?

In most cases, it’s up to you. If you’re married, your spouse may be entitled to a portion of the asset, even if you name someone else as a beneficiary. Otherwise, some popular choices for beneficiaries include:

- Family members, like your spouse, domestic partner, children, parents, or grandchildren.

- Other individuals, including friends and romantic partners. In some states, beneficiaries who inherit from a non-relative may have to pay an inheritance tax on those assets.

- Nonprofits or charities. Many people are surprised to learn you can designate a charity as a beneficiary. It’s a great way to make a lasting impact and support a cause that matters to you.

Keep in mind that minors generally aren’t able to receive property until they become an adult, which is usually at age 18. If you have young children and want to name them as beneficiaries, you may consider the following options:

- Name your children’s legal guardian as the beneficiary, instead of your children themselves. To do this, you must designate a legal guardian for your children in your last will and testament.

- Name a custodian in your beneficiary designation form. A custodian’s job is to manage the financial assets of a specific account for a minor until that minor becomes an adult. For example, say you named a custodian for your life insurance policy. The custodian would manage those funds until your children could take direct ownership.

- Establish a trust for your child and name a trustee to manage the assets. You can state in your will that you want a trust set up after your death. If you were to pass away, the trust would hold your child’s inheritance, and a trustee would manage the assets. With a trust, you have control over when your child receives their inheritance. For example, you might want them to receive a set amount each year until they reach a certain age. You can also name the trust as the beneficiary of a non-probate asset. This would bring all of your assets under one “umbrella,” and your trustee would manage them for the benefit of your child.

There’s a lot to consider if you name a minor as your beneficiary. If you have questions about your personal situation, or if you want to set up a trust to manage your children’s inheritance, consider working with an estate attorney.

How to set up beneficiary designations for non-probate assets

We’ve established why designating beneficiaries for your non-probate assets is valuable. So how do you actually go about doing it?

Here’s a simple three-step process to designate beneficiaries for your 401(k) account, life insurance policy, and more:

1. Create a list of your non-probate assets and their corresponding institutions.

For example, perhaps you have a Roth IRA account with Fidelity and a life insurance policy with Nationwide. You may find it helpful to track this information in an Excel spreadsheet or keep a written list alongside your other estate planning documents. Consider including important information, such as the account or policy number. Having this information makes it easier for your loved ones to track down your accounts after you're gone.

Another option is to use an online estate planning tool — like FreeWill — to track your beneficiary designations. We help you organize all your non-probate assets in one place, so you can plan your beneficiary designations easily. Then you can print a single page that lists your beneficiary information, and store it in a safe place with your will and other important documents.

2. Contact each institution where you have non-probate assets to set up your beneficiaries.

There are usually a few ways to set up your beneficiaries, depending on the institution:

- You can call their customer service line and tell them you want to designate or update a beneficiary

- Some institutions provide beneficiary designation forms on their website that you can print, fill out, and mail back

- Other institutions let you set your beneficiary designations through your online account portal

If you use FreeWill’s beneficiary designation platform, we provide step-by-step instructions for how to reach out to each institution, including specific phone numbers and help lines. It’s always a good idea to follow up with your institution to make sure they received and recorded your designation.

3. Add this beneficiary information to your tracking document.

Whether you’re tracking your beneficiary designations electronically or on paper, it’s a good idea to jot down your beneficiary for each account. You should store this information with your personal papers so it’s easy to find after you pass away.

Why is it important to designate beneficiaries for non-probate assets?

If you don’t name beneficiaries for your non-probate assets, you won’t have any control over who inherits them. Many institutions will list a default beneficiary, like your children or estate. However, it will take time to determine who should receive the assets, which will delay how quickly your loved ones can access and use them.

It’s also the beneficiary’s responsibility to claim ownership of a non-probate asset. So if no one knows the asset exists, or doesn’t know who should inherit it, it could get caught in probate, inaccessible to your loved ones who may need it. That’s a confusing situation that you can avoid by designating beneficiaries and keeping record of this information.

You’ve made your beneficiary designations — now what?

Designating beneficiaries isn’t enough — you also need to keep them updated. As your life changes over time, it’s normal for your beneficiary preferences to change as well. If you don’t update your beneficiary designations, your assets could go to beneficiaries you no longer want to receive them — like an ex-spouse.

Beneficiary designations override what’s written in your will, so it’s important to keep them up to date. For example, say you wrote your ex-spouse out of your will after you got divorced, but left them as the beneficiary on your life insurance policy. They may be entitled to that payout after you die, even if there are other people you wanted to receive it. That’s why it’s important to review your beneficiary designations often and keep them current.

Estate planning professionals recommend reviewing your estate planning documents — including your beneficiary designations and your will — every three to five years, or after any major life events.

If you designate beneficiaries for your assets, do you still need a will?

Yes — it’s always a good idea to have a last will and testament! Only certain assets are able to skip probate. Any other assets you own — including your home, vehicles, and even your pets — will likely have to go through the probate process. Having a will saves time, money, and stress for your loved ones. It’s a powerful legal document that lets you protect the things that matter to you. For example, if you have minor children, you can use a will to name a guardian for them if you pass away.

Not sure you need a will? Here are ten important reasons to have one.

Designating beneficiaries provides peace of mind

The average middle-aged adult has more than five non-probate assets. Choosing beneficiaries for these assets is an important part of estate planning. It eliminates confusion and makes it easier for you to pass on your property to the people and organizations you love. FreeWill’s beneficiary designation platform will walk you through the process in just a few minutes.

Make your free estate plan today

Make your free advance healthcare directive

Make your free durable power of attorney

Make a stock donation today

Make your free revocable living trust